AI Productivity Gains Are Not Enough: Why Companies Need New Business Models

The technologies that change society are not the ones that simply cut labor cost. They are the ones that raise the marginal productivity of ordinary workers across sectors.

The story most people tell about industrialization is too tidy. Machines improved efficiency, firms scaled, profits rose, and society got richer. That happened. But it skips the mechanism that actually mattered. The industrial age changed society when technology increased what one worker could make happen in an hour — not just what one owner could extract from a payroll.

The great breakthroughs were not isolated inventions. They were general-purpose technologies that spread across sectors, kept getting cheaper, and forced complementary changes everywhere else: transport, energy, health, education, how organizations were structured. That is why their gains did not stay locked inside a few firms. (NBER)

Steam let workers command more power than muscle or animal traction ever could. Rail then widened the market — which mattered more than most strategy decks admit. Larger markets made deeper specialization worthwhile, and greater market access raised productivity in manufacturing as rail networks expanded. Electricity then reorganized production again. It was not just a cleaner energy source. It changed the architecture of the factory and the city. Power could be distributed machine by machine, hour by hour, building by building.

The lesson I take from rail and electricity is simple: productivity surges came when a technology changed the reachable scale of the worker, not merely the efficiency of the firm. (NBER)

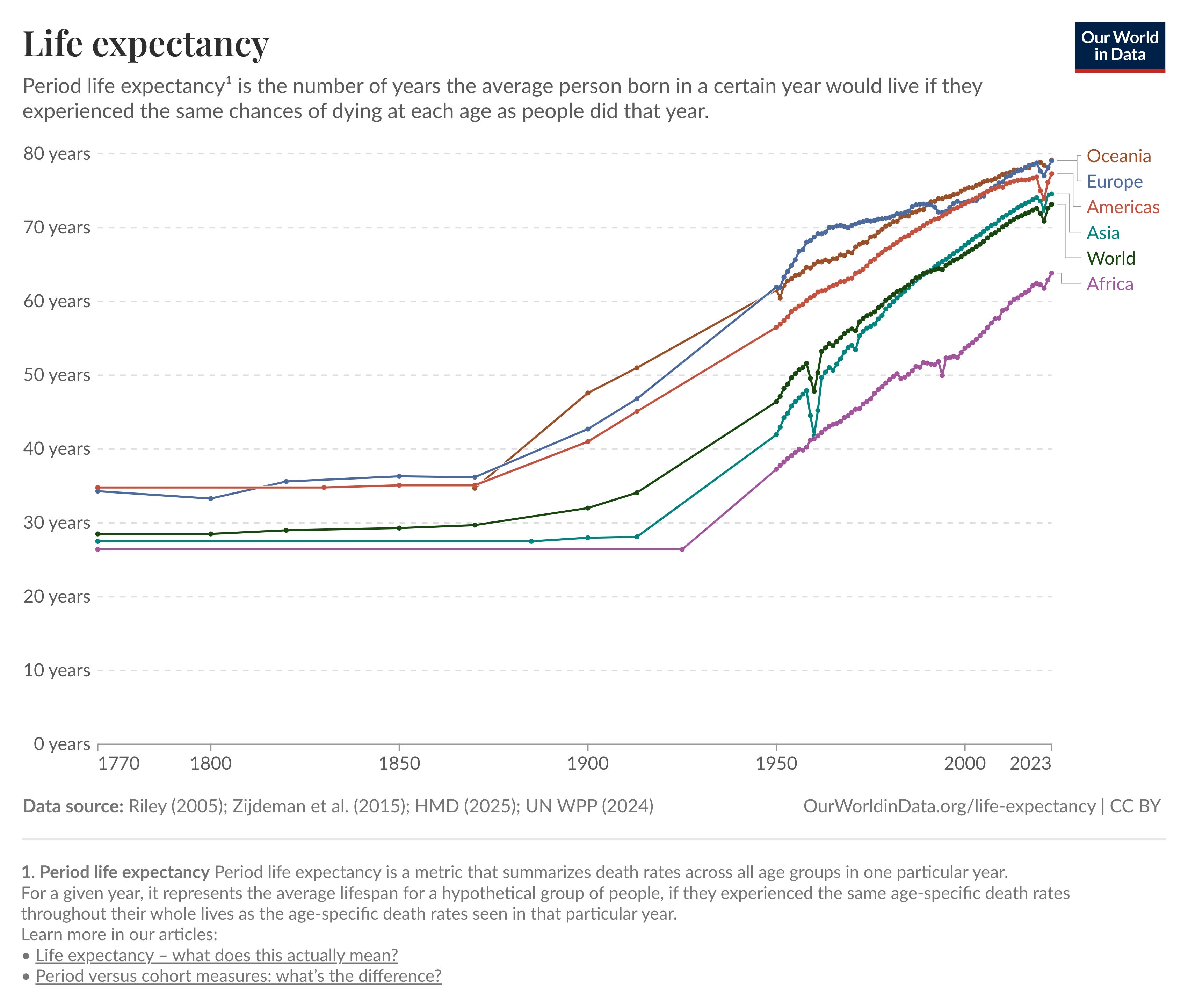

The same was true outside the factory. Sanitation and public health made labor more reliable. Life expectancy has more than doubled globally over the last two centuries, and that was not a side effect — a healthier population is a more dependable workforce, a more educable society, and a broader base for consumption and saving. Historical evidence from Prussia and later industrial Europe shows that schooling and literacy were not ornamental. They were part of the adoption mechanism. New tools diffuse only when enough people can operate, maintain, adapt, and reorganize around them. That was true in the nineteenth century. It is still true now. (Our World in Data)

The Category Error Most Executives Are Making

This category error is one reason why AI investment is distorting innovation capital allocation.

I keep coming back to this history because a lot of the AI conversations I am in make the same category error that earlier generations could have made with electrification. The technology is being treated mainly as a labor-reduction tool. That is a profit story, not yet a civilization story.

The dominant framing goes like this: use AI to do more with fewer people, compress costs, protect margins. It is not wrong. It just stops too early. Electrification did not just make existing factories cheaper to run. It made entirely new industries possible — industries that had no predecessor and could not have existed under the previous energy regime. The candle factory did not get optimized. It got replaced by something that operated on a different logic entirely.

The same fork is available now. Companies that treat AI as a cost lever will capture efficiency gains inside their current business model. Cost reduction may improve the current model, but business model validation must test the whole system. Companies that treat it as a general-purpose technology will ask a different question: what can we now do, deliver, or offer that was previously economically impossible? New revenue streams, new customer relationships, new categories. That is not an incremental improvement on what already exists. It is a different bet entirely.

Most of the AI investment I see is going into the first path. That is understandable — the returns are visible, the timeline is short, the board presentation writes itself. But it is the narrower opportunity, and it carries a hidden risk: you optimize yourself into a position that a competitor with a bolder model can undercut or bypass entirely.

OECD analysis suggests AI could add roughly 0.5 to 1 percentage point to annual labor productivity growth across G7 economies over the next decade. The IMF estimates almost 40 percent of global employment is exposed. Those numbers are large enough to matter — but they do not tell us whether the gains will be broad or narrow, or whether they will show up as cost savings inside old models or as revenue from new ones. (OECD) (IMF)

Diffusion Is Real. Redesign Is Not.

Before funding the next AI bet, leaders need to ask whether they have corporate innovation readiness before funding new bets.

The first real signal is that AI is spreading, but unevenly. As of late 2025, 17 percent of US businesses reported using AI in business functions, with far higher usage among larger firms and in information, finance, insurance, and professional services. Stanford’s AI Index 2025 points to a growing body of evidence that AI can boost productivity and narrow skill gaps in some tasks. That is the hopeful reading. The less comfortable reading is that diffusion is still partial, firm capabilities are uneven, and aggregate gains remain uncertain — because adoption without redesign usually disappoints. We learned that with electrification. We learned it again with computing. Buying the tool is not the same as rebuilding work around it. (Federal Reserve)

The firms getting the most out of AI right now are not simply running the same processes faster. They are changing what they offer, how they price it, and who they can serve. A law firm that uses AI to cut associate hours by 30 percent has an efficiency gain. A legal services firm that uses AI to offer subscription-based contract management to mid-market companies that previously could not afford legal support has a new business. The underlying technology is the same. The ambition is not.

AI Is Not Arriving Alone

What makes this moment more interesting than the usual commentary suggests is that AI is not arriving alone. It is arriving alongside cheaper energy technologies, falling battery costs, denser robot deployment, better sensors, and far more software-mediated coordination. The IEA expects global solar investment to hit roughly $450 billion in 2025, making it the single largest line item in global energy investment. Lithium-ion battery pack prices fell 20 percent in 2024, the sharpest drop since 2017. In other words, the cost of machine power is falling again while the cost of machine cognition is also falling. That combination is more historically significant than the chatbot discourse. (IEA)

Robotics is becoming less exceptional and more infrastructural. Western Europe reached a record robot density of 267 industrial robots per 10,000 manufacturing employees in 2024, ahead of North America at 204. Five countries — China, Japan, the US, South Korea, and Germany — accounted for 80 percent of global installations. This does not mean humanoids are about to flood every workplace. It means the installed base of machine capability is steadily rising, especially where repetitive, high-precision, or hazardous work can be standardized. Once AI improves machine perception and coordination, robotics stops being a capital goods story and becomes part of a worker-leverage story. One technician, operator, planner, or nurse can supervise more assets, handle more complexity, and deliver more output. (IFR)

Where the Near-Term Gains Will Actually Show Up

The next productivity wave will not come from AI replacing whole professions in one dramatic move. It will come from intelligence becoming a cheap layer inside thousands of workflows. The near-term winners will be workers who can direct, check, combine, and escalate machine output — not those who merely sit beside it. The strongest gains will likely show up where cognition is repetitive but high value, where decisions require synthesis across many documents or signals, where coordination delays are costly, and where labor shortages already constrain output. Law, engineering, sales, procurement, logistics, health administration, industrial maintenance, design, parts of education — all fit that pattern. (OECD)

Over the next five years, the most important shift will be from tools that answer questions to systems that complete bounded sequences of work. That will raise output for some workers and compress demand for others, especially in entry-level cognitive tasks that exist mainly to process information for somebody higher up. Some job ladders will get damaged before new ones are built. The social risk is not only unemployment. It is a narrower route into skilled work. If firms automate away the apprenticeship layer, they may save cost now and weaken their talent formation later. The industrial age produced broad gains because it built capability at scale. A future that strips away learning pathways could raise profits while shrinking mobility. That is a real choice, not an inevitability. (IMF)

The Longer Game

Over the next ten to fifteen years, the bigger story is likely to be the convergence of cheap intelligence, cheap electricity, storage, and robotic execution. More sectors will be able to automate not just analysis but physical throughput. Warehouses, ports, energy systems, factories, labs, fragments of care work — all more software-defined. The societies that benefit most will not be those with the best frontier models. They will be the ones that diffuse capability into ordinary firms, train workers fast, expand grid and data infrastructure, and keep access broad enough that productivity gains are not restricted to capital-rich incumbents. (OECD)

My bet on the real frontier further out: the fusion of intelligence with matter. AI for design, simulation, biology, materials, manufacturing, and grid orchestration is more consequential than AI for prettier slides. That is where new industries form, where marginal productivity can jump in ways society actually feels — cheaper energy, faster drug development, more adaptive production, less waste, more output per worker in sectors that still feel stubbornly physical. And that is exactly where the general-purpose argument becomes most visible: the companies building in those spaces are not optimizing existing revenue. They are creating categories that did not exist before.

The Standard That Matters

The real test for this wave is not whether AI can write a memo. Not whether a company can cut headcount and call it transformation. The question is whether the new stack makes ordinary workers economically stronger across many industries — and whether enough firms are willing to ask what becomes possible rather than just what becomes cheaper.

The industrial age did not matter because it automated work. It mattered because it multiplied the force of labor and opened doors to industries no one had named yet. That is the standard the next one will be judged by too.